Canada’s Federal Tax Brackets for 2025

Canada’s federal government sets one set of brackets that applies to every Canadian, in every province. Here are the official 2025 rates from the Canada Revenue Agency (CRA):

SOURCE: Canada Revenue Agency — Taxtips.ca 2025 Federal Rates | H&R Block Canada

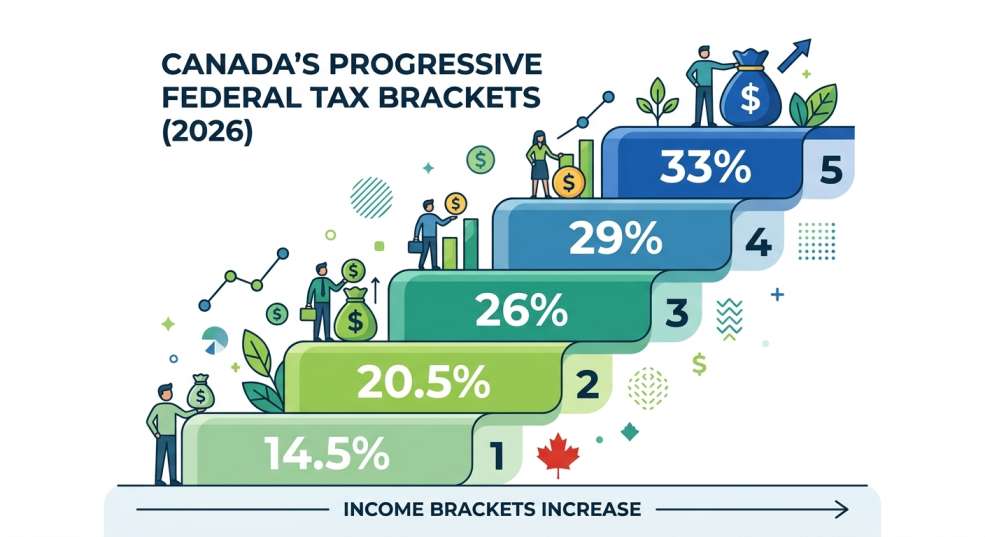

TABLE 1: 2025 Federal Income Tax Brackets — Canada

| Taxable Income Range | Federal Tax Rate |

|---|---|

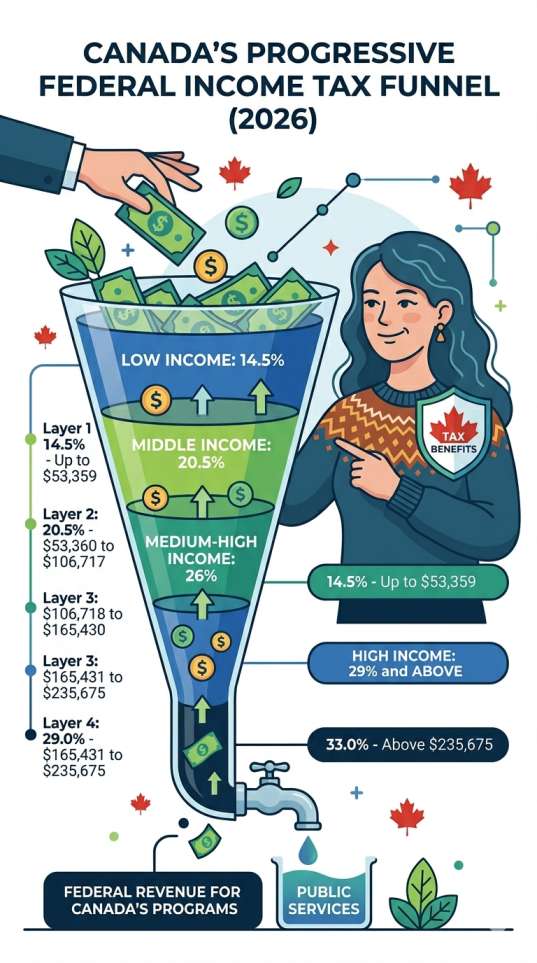

| $0 – $57,375 | 14.5% |

| $57,375 – $114,750 | 20.5% |

| $114,750 – $177,882 | 26% |

| $177,882 – $253,414 | 29% |

| Over $253,414 | 33% |

Source: Canada Revenue Agency (CRA), 2025 tax year. taxtips.ca

Important note for 2025: The lowest federal bracket dropped from 15% to an effective 14.5% this year (because the rate cut from 15% to 14% was applied starting July 1, 2025). Starting in 2026, it becomes a flat 14%. This is a meaningful tax cut for lower and middle-income earners — including most newcomers in their first working years.

The Basic Personal Amount — Your Free Pass

Before you pay a single dollar of federal tax, the CRA gives everyone — newcomers included — a Basic Personal Amount (BPA) of $16,129 for 2025. This is the amount of income you can earn completely tax-free at the federal level.

This means if you earned $16,129 or less in 2025, you owe zero federal income tax. Most newcomers who work part of the year (because they arrived mid-year) will find this especially valuable.

Credits and Deductions Newcomers Often Miss

Filing taxes isn’t just about what you owe — it’s about what you’re owed. Canada has a generous system of credits and deductions, many of which newcomers qualify for immediately.

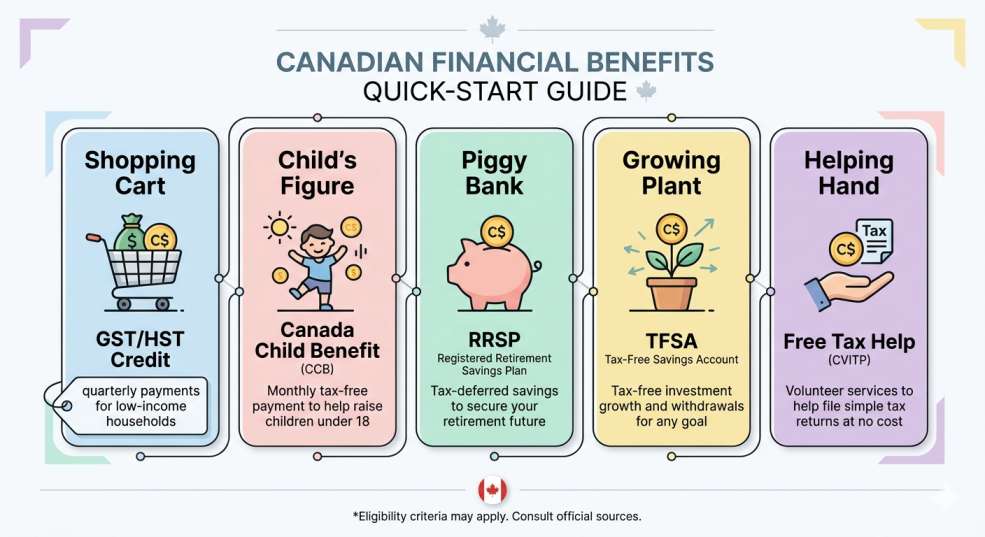

The GST/HST Credit

Once you file your first tax return, the CRA automatically assesses whether you qualify for the GST/HST credit — a quarterly, tax-free payment to offset consumption taxes. For 2025, eligible individuals can receive hundreds of dollars annually depending on income and family size. You don’t apply separately — just file your return and the CRA determines eligibility.

Canada Child Benefit (CCB)

If you have children under 18, the Canada Child Benefit could be one of the most significant financial benefits available to your family. It’s a monthly, tax-free payment, and the amount depends on your income and number of children. Many newcomer families are surprised to learn how substantial this benefit can be.

RRSP Contributions

A Registered Retirement Savings Plan (RRSP) is one of Canada’s most powerful tax tools. Contributions you make reduce your taxable income dollar-for-dollar. If Priya from our example above had contributed $5,000 to an RRSP, her taxable income would have dropped to $11,371, reducing her federal tax further.

Your RRSP contribution room is 18% of your previous year’s earned income, up to an annual maximum. As a newcomer, you typically begin accumulating RRSP room after your first year of Canadian income.

TFSA — The Tax-Free Savings Account

A Tax-Free Savings Account (TFSA) doesn’t reduce your taxes on the way in, but any investment growth or withdrawals are completely tax-free. Newcomers who become residents of Canada at age 18 or older can begin contributing immediately. As of 2025, the annual contribution limit is $7,000, with cumulative room that builds each year.

Free Tax Help — CVITP

The Community Volunteer Income Tax Program (CVITP), offered through the CRA, provides free tax preparation help to eligible individuals — including newcomers with modest incomes. Local settlement agencies, community centres, and libraries often host CVITP clinics during tax season.

Source: CRA CVITP Program

Common Mistakes Newcomers Make at Tax Time

Even well-prepared newcomers sometimes stumble. Here’s what to watch for:

1. Assuming you don’t need to file because your income was low. Even with no income, filing can unlock benefits like the GST credit and CCB. Always file.

2. Not declaring foreign income. Canada taxes residents on worldwide income. If you had investment income, rental income, or other earnings in your home country after becoming a Canadian resident, it generally needs to be reported. There may be tax treaty protections — consult a tax professional.

3. Missing your arrival date on the return. Your T1 return includes a field for your date of entry into Canada. This affects how prorated credits are calculated.

4. Confusing marginal rate with effective rate. Your marginal rate (the rate on your last dollar) is NOT what you pay on your entire income. Your effective rate is almost always lower.

5. Not setting up direct deposit with the CRA. Register your bank account through CRA My Account to receive any refunds and benefits faster — directly into your account.

Practical Takeaways — Your Tax Checklist as a Newcomer

Here’s a quick-reference summary of everything you need to do:

Get your SIN number (Service Canada)

Get your SIN number (Service Canada)- Keep records of your Canadian arrival date

- Understand the two-layer system: federal + provincial tax

- Know your Basic Personal Amount ($16,129 federally for 2025)

- File your return by April 30 — even if income was minimal

- Apply for GST/HST Credit and Canada Child Benefit (by filing)

- Explore RRSP contributions in your second year

- Open a TFSA as soon as you become a resident

- Look for a free CVITP tax clinic in your community

- Register for CRA My Account online

Conclusion: Taxes Are a Sign You Belong Here

Canada’s tax system might look intimidating at first glance, but once you understand the logic, it’s genuinely designed to be fair. The progressive bracket structure means you’re only taxed heavily on the income you’ve truly earned above certain thresholds. The benefits system — CCB, GST credits, TFSA, RRSP — is robust enough that many newcomers actually receive more from the government than they owe in their first year.

More importantly, filing taxes in Canada is your gateway to the full suite of programs this country offers. It’s how the government knows you’re here, how you access healthcare subsidies, how you build credit history and financial standing as a new resident.

You came to Canada to build a better life. Understanding how your money works — including how you’re taxed and what you get back — is one of the most practical steps toward doing exactly that.

Welcome to Canada. Now go file that return.