Let’s be real. Most Canadians grew up hearing that investing was complicated — something you handed off to a bank advisor, crossed your fingers, and hoped for the best. The idea of picking stocks felt intimidating, mutual fund fees felt murky, and the whole thing seemed designed for people who already had money.

But there’s a middle ground that millions of Canadians have quietly discovered, and it’s changing the way everyday people build wealth: Exchange-Traded Funds, or ETFs.

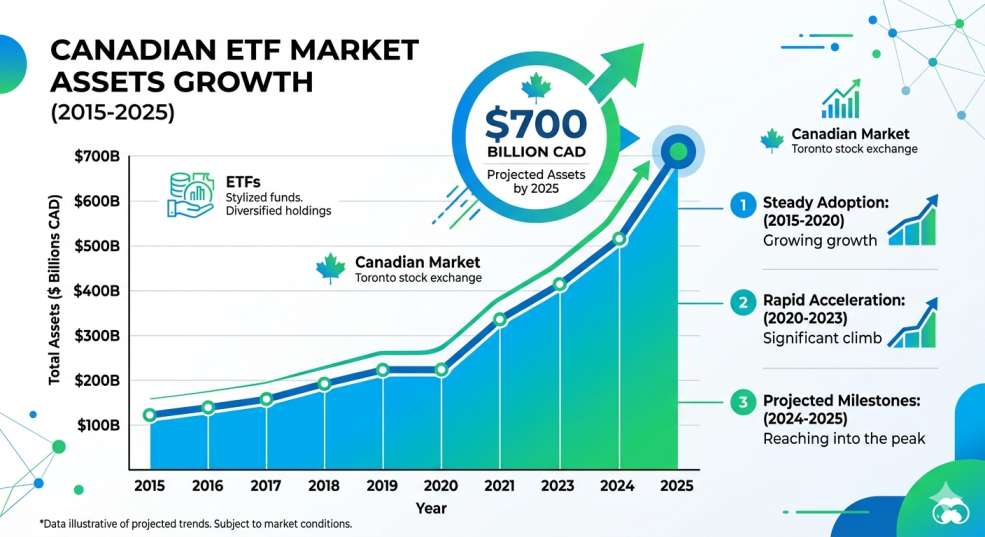

ETFs are not a new invention — they’ve been around since the 1990s — but they’ve exploded in popularity, especially in Canada. In fact, Canadian ETF assets hit the $700 billion milestone in 2025, according to TD Securities, fuelled by record inflows of $122 billion in a single year. That kind of growth doesn’t happen by accident. ETFs are genuinely one of the most accessible, cost-effective, and flexible ways to invest — whether you’re starting with $500 or $500,000.

This guide breaks down exactly what ETFs are, how they work in the Canadian context, how to choose the right ones, and how to get started — even if you’ve never bought a single investment in your life.

What Is an ETF? The Simple Explanation

An Exchange-Traded Fund (ETF) is essentially a basket of investments — like stocks, bonds, or commodities — that you can buy and sell on a stock exchange, just like a single stock.

Think of it this way: instead of buying one stock in one company (say, a Canadian bank), you buy one ETF that holds shares in hundreds or thousands of companies simultaneously. When the market goes up, your ETF goes up. When it goes down, it goes down — but because you’re diversified across many companies and sectors, the impact of any single company failing is dramatically reduced.

ETFs typically track an index — a list of investments that follows a specific market segment. The S&P/TSX Composite Index, for example, tracks the largest companies listed on the Toronto Stock Exchange. When you buy an ETF that tracks that index, you’re getting exposure to all of those companies in one single purchase.

How ETFs Differ from Mutual Funds

Canadians are very familiar with mutual funds — they’ve been sold through banks for decades. But ETFs have several meaningful differences:

- Traded like stocks: ETFs trade throughout the day on an exchange. Mutual funds are priced once daily after markets close.

- Lower fees: ETF management expense ratios (MERs) are dramatically lower than traditional mutual funds, often 10x cheaper.

- Transparency: You can see exactly what an ETF holds at any time. Mutual fund holdings are disclosed less frequently.

- No minimums (generally): You can buy a single share of most ETFs. Some mutual funds require minimum investments of $500–$1,000 or more.

Why ETFs Have Become the Go-To Investment for Canadians

The appeal of ETFs goes beyond just being “cheaper than mutual funds.” Here’s why they resonate so strongly with Canadian investors:

1. Instant diversification. One ETF can hold hundreds of companies across multiple countries and sectors. A single all-in-one ETF can give you exposure to Canadian, U.S., and international stocks plus bonds — all in one ticker.

2. Low cost. Fees matter enormously over time. A mutual fund with a 2% MER versus an ETF with a 0.20% MER might not sound like much, but over 30 years, that difference can cost you tens of thousands of dollars.

3. Tax efficiency. ETFs generate fewer taxable events than actively managed funds, making them particularly effective inside tax-sheltered accounts like the TFSA and RRSP.

4. Simplicity. You don’t need to analyze earnings reports or predict where the economy is headed. You just invest regularly and let compounding do the heavy lifting.

5. Accessibility. With platforms like Wealthsimple Trade, you can start investing in ETFs commission-free with as little as a single share.

Types of ETFs Available to Canadian Investors

Not all ETFs are the same. Understanding the major categories helps you choose what fits your goals.

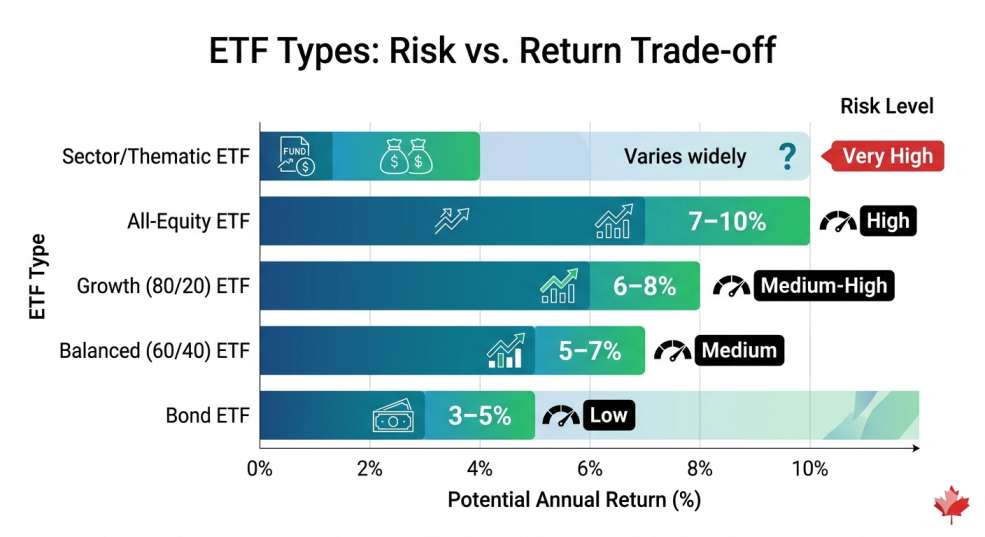

Equity ETFs

These hold stocks and are designed for growth. They can track broad markets (like the entire Canadian stock market), specific sectors (tech, energy, financials), or specific countries.

Examples:

- VCN (Vanguard FTSE Canada All Cap Index ETF) — broad Canadian market

- VFV (Vanguard S&P 500 Index ETF) — U.S. stocks in Canadian dollars

- XAW (iShares Core MSCI All Country World ex Canada Index ETF) — global diversification outside Canada

Bond ETFs

These hold fixed-income securities like government or corporate bonds. They typically offer lower returns but more stability — useful for conservative investors or as a portfolio balancer.

Examples:

- ZAG (BMO Aggregate Bond Index ETF)

- XBB (iShares Core Canadian Universe Bond Index ETF)

All-in-One / Asset Allocation ETFs

These are the “set it and forget it” option and have become incredibly popular in Canada. A single ETF holds a diversified mix of stocks and bonds across multiple countries, automatically rebalanced.

Examples:

- VEQT — Vanguard All-Equity ETF Portfolio (100% stocks, aggressive growth)

- XEQT — iShares Core Equity ETF Portfolio (100% stocks)

- VGRO — Vanguard Growth ETF Portfolio (80% stocks / 20% bonds)

- XBAL — iShares Core Balanced ETF Portfolio (60% stocks / 40% bonds)

Sector & Thematic ETFs

These focus on specific industries or trends — like clean energy, technology, gold, or real estate. They carry more risk but can complement a core portfolio.

REIT ETFs

Real Estate Investment Trust ETFs give you exposure to real estate without owning property. Useful for generating dividend income.

Note: Returns are historical approximations, not guarantees. Source: Vanguard Canada, iShares Canada product pages.

TABLE 1: Popular Canadian ETFs for Beginners (2025 Data)

| ETF Ticker | Name | Provider | MER | Type | Best For |

|---|---|---|---|---|---|

| VEQT | All-Equity ETF Portfolio | Vanguard | 0.24% | All-Equity | Long-term growth investors |

| XEQT | Core Equity ETF Portfolio | iShares | 0.20% | All-Equity | Low-cost equity exposure |

| VGRO | Growth ETF Portfolio | Vanguard | 0.25% | 80/20 Growth | Growth with some stability |

| XGRO | Core Growth ETF Portfolio | iShares | 0.20% | 80/20 Growth | Slightly lower cost growth |

| VBAL | Balanced ETF Portfolio | Vanguard | 0.25% | 60/40 Balanced | Moderate risk tolerance |

| ZBAL | BMO Balanced ETF | BMO | 0.20% | 60/40 Balanced | BMO ecosystem users |

| VCN | FTSE Canada All Cap | Vanguard | 0.05% | Canadian Equity | Canadian market exposure |

| VFV | S&P 500 Index ETF | Vanguard | 0.09% | U.S. Equity | U.S. market exposure |

| ZAG | Aggregate Bond Index | BMO | 0.09% | Bonds | Conservative/income focus |

Sources: Vanguard Canada, iShares Canada, BMO ETF product pages. MERs as of late 2025. MERs are subject to change.

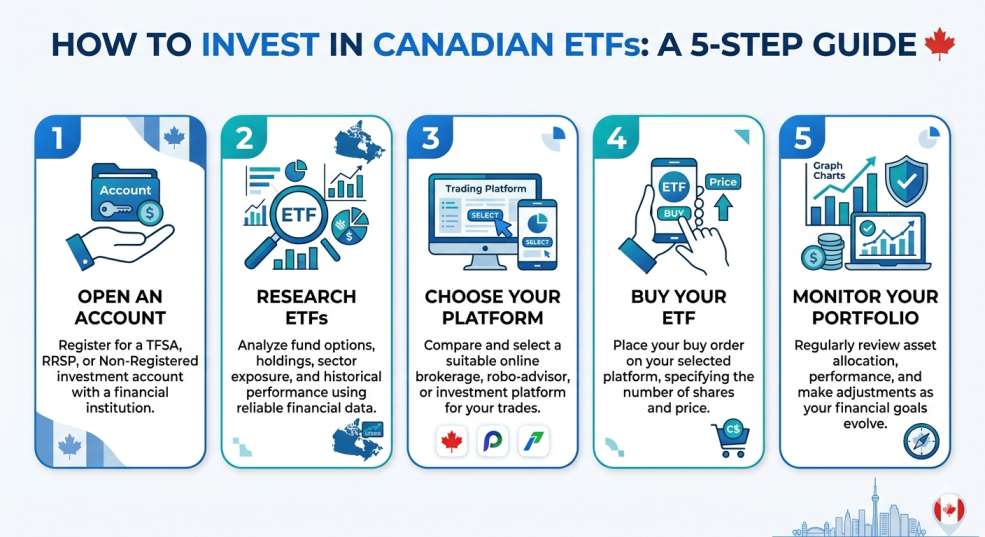

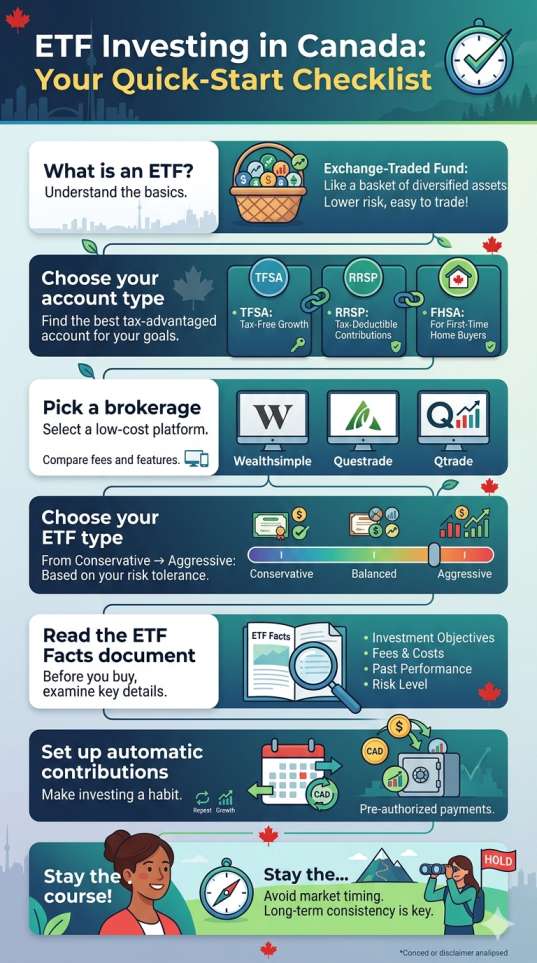

How to Invest in ETFs in Canada: A Step-by-Step Guide

Step 1: Choose the Right Account

Before you buy a single ETF, you need to decide where you’ll hold it. In Canada, your account choice has major tax implications.

TFSA (Tax-Free Savings Account)

- Contributions grow and can be withdrawn completely tax-free

- 2025 contribution limit: $7,000 per year (lifetime room varies by birth year)

- Best for: flexible goals, emergency funds, medium-to-long-term investing

- Learn more at the CRA TFSA page

RRSP (Registered Retirement Savings Plan)

- Contributions are tax-deductible (reduces your taxable income now)

- Investments grow tax-deferred until withdrawal (ideally in retirement)

- Contribution limit: 18% of previous year’s earned income (up to an annual maximum)

- Best for: retirement savings, especially if you’re in a higher tax bracket now

- Learn more at the CRA RRSP page

FHSA (First Home Savings Account)

- New as of 2023 — designed to help first-time buyers save for a home

- Contributions are tax-deductible; withdrawals for a qualifying home purchase are tax-free

- Contribution limit: $8,000/year, $40,000 lifetime

Non-Registered (Taxable) Account

- No contribution limits, no tax sheltering

- Capital gains, dividends, and interest are taxable

- Best used after maxing out registered accounts

Most beginners should prioritize filling their TFSA first, then RRSP. ETFs inside a TFSA grow 100% tax-free — that’s a genuinely powerful advantage over a lifetime of investing.

💡 PRO TIP

Step 2: Pick a Brokerage or Investment Platform

You’ll need an account with a platform that lets you buy and sell ETFs. Here are the main options for Canadians:

Discount Brokerages (DIY):

- Wealthsimple Trade — Commission-free trading, excellent app, great for beginners

- Questrade — Free ETF purchases (sell commissions apply), robust platform

- Qtrade — Well-regarded for customer service and research tools

- TD Direct Investing, RBC Direct Investing — Bank-affiliated, higher fees but familiar

Robo-Advisors (Hands-Off):

- Wealthsimple Invest — Builds and manages a diversified ETF portfolio for you

- Justwealth, Nest Wealth — Other strong options with goal-based features

If you’re comfortable doing a little research and want to minimize fees, a discount brokerage + all-in-one ETF (like VEQT or XEQT) is an excellent combination. If you prefer to just set up automatic contributions and forget about it, a robo-advisor is worth the slightly higher fee.

Step 3: Research and Choose Your ETFs

For most Canadian beginners, the all-in-one ETF approach is the smartest starting point. It provides instant global diversification, automatic rebalancing, and requires almost no maintenance.

Here’s a simple framework based on your investment timeline and risk tolerance:

- Aggressive (10+ year horizon, comfortable with volatility): VEQT or XEQT (100% equities)

- Growth (7–10 year horizon): VGRO or XGRO (80/20 stocks/bonds)

- Balanced (5–7 year horizon): VBAL or XBAL (60/40 stocks/bonds)

- Conservative (under 5 years): VCNS or XCNS (40/60 stocks/bonds) or a bond ETF

For more advanced investors looking to build a multi-ETF portfolio, a common Canadian strategy is the “Three-Fund Portfolio”: one Canadian equity ETF (e.g., VCN), one U.S. equity ETF (e.g., VFV), and one international/bond ETF (e.g., XAW or ZAG). This approach gives you more control over your geographic allocation but requires occasional manual rebalancing.

Step 4: Read the ETF Facts Document

Before buying any ETF in Canada, you’re entitled to an ETF Facts document — a standardized, plain-language summary that covers:

- What the ETF invests in

- Its MER (management expense ratio)

- Historical performance

- Key risks

This document is required by Canadian securities regulators and must be delivered to you when you purchase an ETF for the first time. Always review it before buying.

Step 5: Place Your Order

When you’re ready to buy, log into your brokerage, search for the ETF ticker (e.g., VEQT on the TSX), and place an order.

Order type matters:

- Market order: Buys immediately at whatever the current price is. Quick, but you have less control.

- Limit order: You set the maximum price you’re willing to pay. Slightly more effort, but protects you from sudden price spikes, especially for ETFs with lower trading volumes.

Best time to trade: Avoid the first and last 15 minutes of the trading day when spreads (the gap between buy and sell prices) tend to be widest. Mid-morning or midday typically offers better pricing.

Step 6: Automate and Stay Consistent

The most powerful thing you can do after your first purchase is set up automatic contributions. Dollar-cost averaging — investing a fixed amount on a regular schedule, regardless of market conditions — is one of the most battle-tested wealth-building strategies in personal finance.

Contributing $300/month automatically removes the temptation to time the market (which almost never works), keeps your investing consistent, and lets compounding do its job.

TABLE 2: TFSA vs. RRSP vs. FHSA — Which Account for Your ETFs?

| Feature | TFSA | RRSP | FHSA |

|---|---|---|---|

| Tax on Growth | Tax-free | Tax-deferred | Tax-free (for home purchase) |

| Tax Deduction for Contributions | No | Yes | Yes |

| Withdrawal Rules | Anytime, no tax | Taxable on withdrawal | Tax-free for first home only |

| 2025 Contribution Limit | $7,000/year | 18% of income (max ~$31,560) | $8,000/year ($40,000 lifetime) |

| Who It’s Best For | Most Canadians | Higher earners planning retirement | First-time homebuyers |

| Can Hold ETFs? | Yes | Yes | Yes |

Source: Canada Revenue Agency (CRA). Contribution limits are subject to change annually.

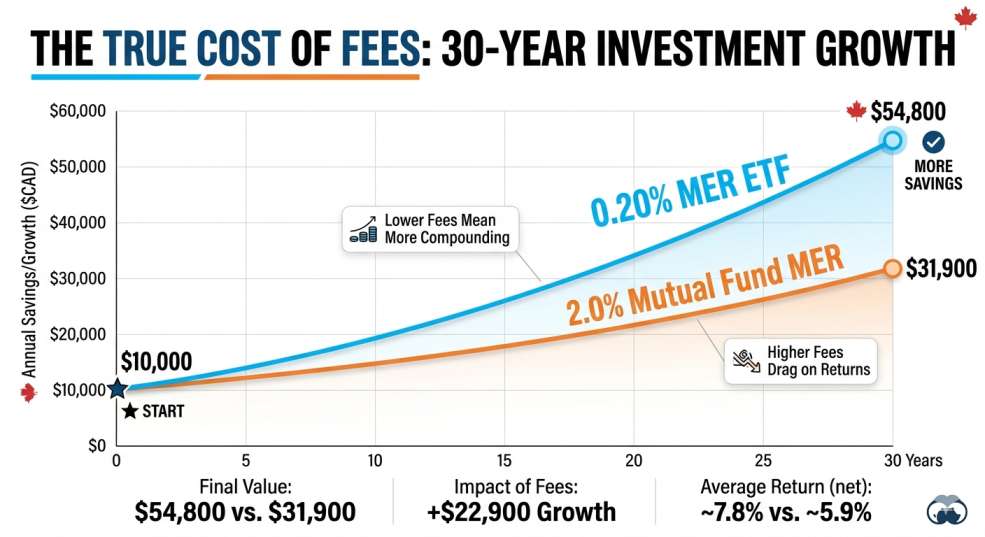

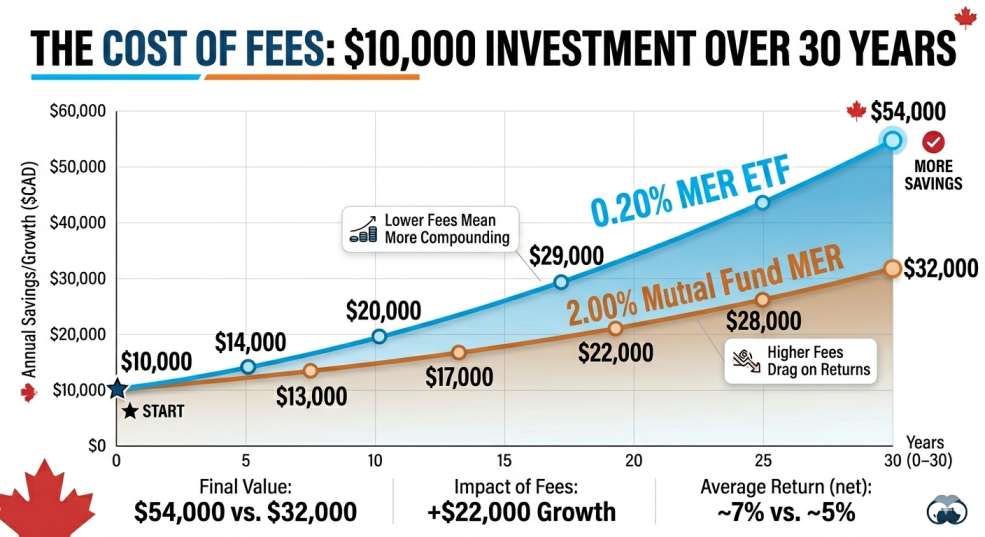

Understanding ETF Fees: Why They Matter More Than You Think

The Management Expense Ratio (MER) is the annual fee charged by an ETF provider, expressed as a percentage of your total investment. It’s deducted automatically — you never see it as a separate bill, but it quietly affects your returns every single year.

Here’s why this matters dramatically over time:

Imagine you invest $10,000 and earn 7% annually before fees.

- At 0.20% MER (typical ETF): After 30 years → ~$54,000

- At 2.00% MER (typical actively managed mutual fund): After 30 years → ~$32,000

That’s a $22,000 difference from fees alone. On the same investment. Over the same time period.

This isn’t a theoretical argument against all mutual funds — some actively managed funds do outperform, particularly over shorter periods. But the research is clear: over long periods, the majority of actively managed funds underperform their benchmark index after fees. (Source: SPIVA Canada Scorecard, S&P Dow Jones Indices)

The good news for Canadian investors: competition among ETF providers has been fierce, and fees keep dropping. In late 2025, Vanguard Canada made its biggest fee cut in history, bringing its all-equity portfolio (VEQT) to a 0.24% MER — and iShares and BMO have similarly competitive pricing on their core offerings.

Note: Hypothetical illustration only. Does not account for taxes or transaction costs.

Common Mistakes Canadian ETF Investors Make (And How to Avoid Them)

Even a simple investment like an ETF can be undermined by a few common errors:

1. Checking your portfolio too often.

Markets fluctuate daily, sometimes dramatically. Investors who obsessively track their portfolios tend to panic during downturns and sell at the worst possible time. Set up your contributions, check in quarterly, and let time do the work.

2. Chasing last year’s top performers.

The gold ETF that returned 50% last year is not guaranteed to do the same next year. Building a core portfolio around broad, diversified ETFs is more reliable than rotating into whatever recently performed best.

3. Ignoring currency risk.

When you buy a U.S.-listed ETF (like SPY on the NYSE), your returns are subject to USD/CAD exchange rate fluctuations. Buying the Canadian-listed version of a U.S. ETF (like VFV on the TSX, which holds S&P 500 stocks but trades in CAD) can simplify things — though it doesn’t eliminate currency exposure entirely.

4. Using market orders during volatile periods.

A limit order gives you control over your buy price. This matters especially during fast-moving markets or for ETFs with lower trading volumes.

5. Neglecting to rebalance.

If you’re building your own multi-ETF portfolio, your allocation will drift over time as different assets grow at different rates. Annual rebalancing keeps your risk profile on track. All-in-one ETFs handle this automatically.

A Real-World Scenario: Starting with $5,000 in a TFSA

Let’s put this all together with a concrete example.

Profile: Amara, 28, a newcomer to Canada who recently became a permanent resident. She has $5,000 saved and wants to start investing.

Goal: Long-term wealth building (retirement is 35+ years away). Moderate-to-high risk tolerance.

What she does:

- Opens a TFSA on Wealthsimple Trade (free, no commissions on ETF purchases)

- Transfers $5,000 into the account

- Buys XEQT at ~$35/share (purchases approximately 142 shares)

- Sets up an automatic $200/month contribution

- Reviews her portfolio once per quarter, does nothing else

What happens over time:

At a historical average of ~7% annual return (not guaranteed), Amara’s portfolio could grow to approximately $260,000–$310,000 by retirement — from an initial $5,000 plus consistent contributions, compounded over decades.

The key: she doesn’t need to be an expert. She doesn’t need to watch the market daily. She just needs to start, stay consistent, and avoid panic-selling during downturns.

Conclusion: The Best Time to Start Was Yesterday. The Second Best Is Now.

ETFs have genuinely democratized investing in Canada. You no longer need a financial advisor, a big lump sum, or an MBA to build a solid, diversified portfolio. You need a TFSA or RRSP, a brokerage account, one well-chosen ETF, and the discipline to contribute consistently.

Here’s a quick summary of what we covered:

- ETFs are baskets of investments traded on stock exchanges — low-cost, diversified, and transparent.

- All-in-one ETFs (VEQT, XEQT, VGRO, XBAL) are ideal for most beginners.

- Account choice matters — prioritize your TFSA first, then RRSP, based on your goals.

- MER (fees) compound over time — even a 1% difference can mean tens of thousands of dollars.

- Start simple, automate, and stay consistent — that’s the strategy that works.

The Canadian ETF market is growing for a reason: more Canadians are discovering that you don’t need to hand over your financial future to a bank. You can take control, keep your costs low, and let a diversified, well-structured portfolio grow — year after year.

Whether you’re a newcomer building roots in Canada, a young professional starting out, or someone who finally decided to take investing seriously — ETFs are one of the most powerful tools you have access to. Use them.

Additional Resources

- Canada Revenue Agency — TFSA Overview

- Canada Revenue Agency — RRSP Guide

- Canadian Securities Administrators — Understanding ETF Facts

- SPIVA Canada Scorecard (Active vs. Passive Fund Performance)

- Morningstar Canada — Best ETFs

- TD Securities — 2025 Canadian ETF Recap

Disclaimer

The information provided in this article is for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice. ETF investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. The examples, projections, and scenarios included are hypothetical illustrations only and are not guarantees of any specific investment outcome. Readers should consult a qualified financial advisor or investment professional before making any investment decisions. Always read the ETF Facts document before purchasing any ETF. ArriveThenThrive.ca is not a registered investment advisor.