Picture this: You’ve landed in Canada, found an apartment, and started your new job — but it’s in a suburb with limited transit. Every morning you’re cobbling together bus connections and rideshares just to get to work. A car isn’t a luxury anymore; it’s the key to actually living your Canadian dream.

Here’s the good news: you don’t have to wait years to build a credit history before getting behind the wheel. Canada has a well-developed ecosystem of lenders, banks, and dealership programs designed specifically to help newcomers get approved for a car loan — sometimes with zero Canadian credit history required.

But the process is different from what you may have experienced back home. Knowing what lenders look for, which programs exist, and how to position yourself for the best possible rate can save you thousands of dollars over the life of your loan.

In this guide, we’ll walk you through everything you need to know to get approved for a car loan in Canada as a newcomer — from understanding your eligibility and gathering your documents, to comparing lenders and building credit for the future.

Why Getting a Car Loan as a Newcomer Is Uniquely Challenging

Most Canadians qualify for auto financing based on their Canadian credit score — a three-digit number that tells lenders how reliably they’ve repaid debts in the past. When you arrive in Canada, you start with a blank slate. Even if you had an excellent credit history in your home country, that record generally doesn’t transfer here.

Most Canadian lenders do not recognize international credit history. (Source: Vernon Toyota Newcomer Program)

💡 QUICK FACT

This creates a classic catch-22: you need credit to get a loan, but you need a loan to build credit. Fortunately, Canadian banks and lenders have recognized this gap and created newcomer auto loan programs that evaluate your application differently — looking at income stability, employment, residency status, and down payment rather than relying solely on a credit score.

Who Qualifies as a “Newcomer” for Auto Loan Programs?

Lender definitions vary slightly, but in general, you likely qualify for newcomer-specific auto financing if you fall into one of these categories:

Permanent Residents (PRs): Most banks serve PRs who have been in Canada for up to 3 to 5 years. RBC, for example, covers permanent residents who arrived within the last 12 months under their standard newcomer program, while TD Auto Finance extends coverage to PRs within their first 5 years. (Sources: RBC, TD Auto Finance)

Temporary Foreign Workers (TFWs): RBC covers temporary workers who arrived within the last 48 months; TD Auto Finance covers TFWs within their first 5 years in Canada.

International Students: Ford Credit Canada’s Newcomer Program, for instance, accepts applicants with a valid Study Permit (IMM 1208 or IMM 1442). RBC also extends newcomer eligibility to international students within their first 12 months. (Source: Ford Credit Canada)

Your eligibility window matters. If you’ve been in Canada for 4 years and just discovered these programs, you may still qualify — but don’t wait. Apply while you still fall within the program’s time limits.

💡 PRO TIP

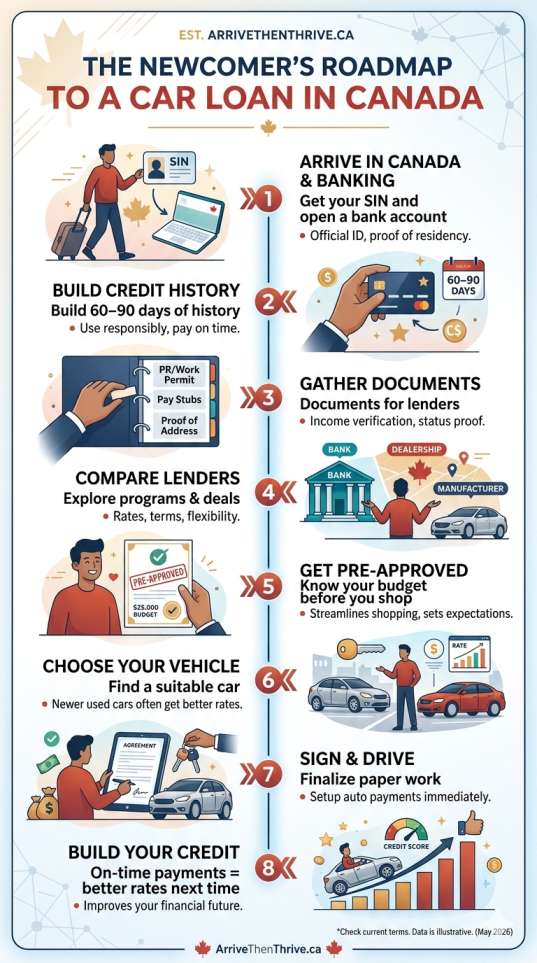

Documents You Need to Apply for a Newcomer Car Loan

One area where newcomers are often caught off guard is documentation. Unlike standard applicants who can rely on a credit pull, newcomer programs require you to prove your identity, residency status, income, and address through physical documents.

Here’s what you’ll typically need:

Identity & Immigration Status:

- Passport (valid)

- Permanent Resident Card (IMM 5688 or IMM 5292), Work Permit (IMM 1102 or IMM 1442), or Study Permit (IMM 1208 or IMM 1442)

- Canadian driver’s licence (if you’ve converted your foreign licence)

Income & Employment:

- Recent pay stubs (typically 2–3 months)

- Employment offer letter or confirmation of employment

- Bank statements showing salary deposits

- If self-employed: business registration documents and bank statements

Proof of Address:

- Utility bill or lease agreement showing your Canadian address

- Recent bank statement with your address

Banking Information:

- A Canadian bank account is essential — most lenders require it for direct debit payments

Note: You must physically be present in Canada and have an established Canadian residential address to apply. (Source: Vernon Toyota)

TABLE 1: Major Canadian Banks & Their Newcomer Auto Loan Programs (2026)

| Lender | Who Qualifies | Max Loan Amount | Max Term | Down Payment Required | Credit History Required |

|---|---|---|---|---|---|

| RBC | PRs (≤12 months), International Students (≤12 months), TFWs (≤48 months) | Up to $75,000 | Up to 96 months | Min. 15% of financed amount | Not required |

| TD Auto Finance | PRs & Foreign Workers (within first 5 years) | Varies by profile | Up to 84 months | May be required | Not required |

| Ford Credit Canada | PRs, TFWs, International Students | Varies | Up to 84 months | Varies | Not required |

| BMO / CIBC / Scotiabank | Varies by program | Varies | Up to 84 months | Varies | May be assessed |

| Subprime / Alternative Lenders | All newcomers including those with no income history | Varies | Up to 96 months | Often higher (20–30%) | Not required |

Sources: RBC, TD Auto Finance, Ford Credit Canada

Note: Program terms change. Always confirm directly with your lender.

Understanding Canadian Car Loan Interest Rates

Interest rates are where newcomers often get hit hardest — and where a little preparation makes a big financial difference.

As of early 2026, the average car loan interest rate in Canada for new vehicles sits around 6.50%, according to Statistics Canada data compiled by Finder Canada. For used vehicles, rates typically range between 8% and 10% for qualified borrowers.

For newcomers with no Canadian credit history, rates will generally be higher — often in the near-prime to subprime range — until you establish a local credit record.

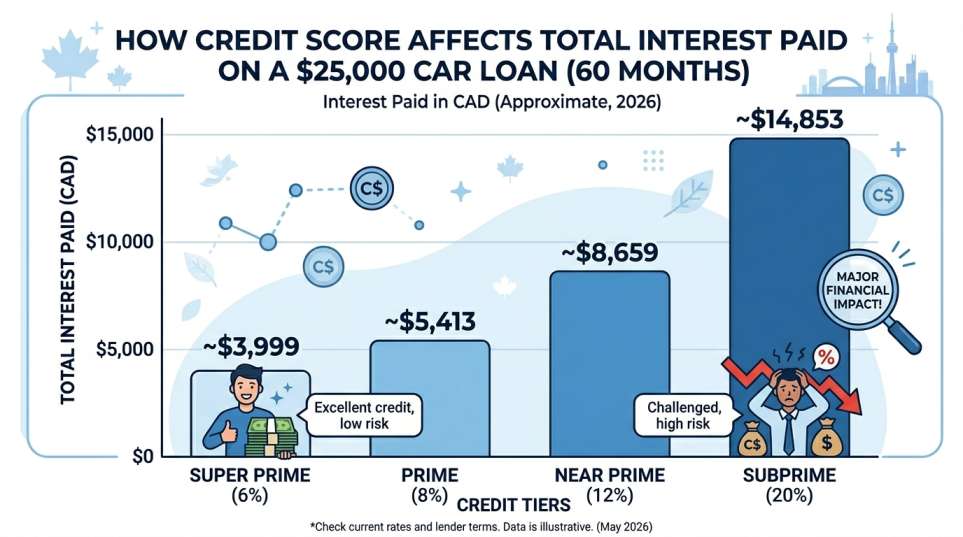

TABLE 2: Car Loan Interest Rates by Credit Profile in Canada (2026)

| Credit Tier | Credit Score Range | Typical Interest Rate | Monthly Payment on $25,000 / 60 months |

|---|---|---|---|

| Super Prime | 720+ | 3.99% – 6.99% | ~$462 – $495 |

| Prime | 670 – 719 | 5.99% – 9.99% | ~$483 – $531 |

| Near Prime | 620 – 669 | 8.99% – 14.99% | ~$519 – $595 |

| Subprime / No History | Below 620 | 10.99% – 29.99%+ | ~$540 – $775+ |

Source: Hello Motors, compiled from Canadian market data 2026

Payments are approximate and for illustration only. Actual rates depend on lender, vehicle age, term length, and individual profile.

As a newcomer, you’ll likely start in the near-prime or subprime tier — but this is temporary. With consistent on-time payments, your credit score will climb and you’ll be eligible for better rates when you refinance or buy your next vehicle.

How to Improve Your Approval Odds Before You Apply

You may not be able to manufacture a Canadian credit history overnight, but there are several proven steps that significantly improve your chances of approval — and reduce the interest rate you’re offered.

Save for a Meaningful Down Payment

A larger down payment reduces the lender’s risk and your loan balance. RBC’s newcomer program, for example, requires a minimum of 15% down. Putting down 20–25% can meaningfully improve your rate and approval odds. On a $30,000 car, a 20% down payment ($6,000) also means you’re financing $24,000 instead of the full amount — reducing both your interest costs and monthly obligations.

Open a Canadian Bank Account and Credit Card First

Before applying for a car loan, open a bank account and apply for a secured credit card or a newcomer credit card with no credit history required. Use it for small purchases and pay the balance in full each month. Even 2–3 months of positive activity begins establishing your Canadian credit file.

Get Pre-Approved Before Visiting Dealerships

Pre-approval from your bank lets you know exactly what you qualify for, giving you negotiating power at the dealership. It also limits unnecessary hard credit inquiries, which can temporarily lower your score. (Source: Ratehub.ca)

Consider a Co-Signer

A Canadian co-signer with an established credit history — such as a relative, spouse, or close friend already settled in Canada — can dramatically improve your approval chances and reduce your interest rate. While not required by all lenders, it’s a valuable option if one is available to you.

Choose a Newer Used Vehicle

Most lenders have restrictions on financing vehicles over 10 years old. Choosing a reliable, lower-mileage vehicle under 7 years old signals lower risk to the lender and may earn you a better rate.

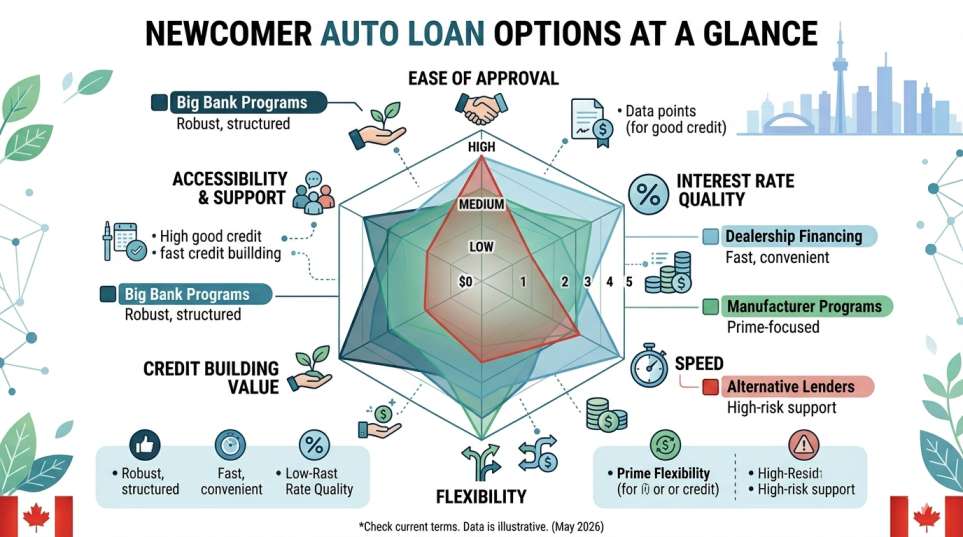

Comparing Your Financing Options: Bank vs. Dealership vs. Alternative Lender

When it comes to securing a newcomer auto loan in Canada, you have three main avenues — and each comes with trade-offs.

Major Bank Newcomer Programs

The Big Five Canadian banks (RBC, TD, BMO, CIBC, Scotiabank) all offer some form of newcomer banking or lending support. RBC and TD have the most robust dedicated newcomer auto loan programs. Rates from major banks typically start around 6.99% to 8.8% for qualified borrowers, with TD Bank’s rates ranging from that band depending on credit score, term, and vehicle type. (Source: Tabangi Motors)

Best for: Permanent residents who have opened a bank account and have some documented Canadian income.

Dealership Financing

Many dealerships work with a network of 10–20+ lenders and can often find approval even when a bank has said no. Dealerships are particularly useful if you have no Canadian credit at all. RBC’s newcomer program, for example, is accessible at over 4,500 dealerships, and TD Auto Finance is available through more than 3,500 dealerships across Canada.

Best for: Recent arrivals who need quick approval and flexibility.

Manufacturer Programs (e.g., Ford Credit, Toyota Financial)

Some automakers have dedicated newcomer financing programs tied to their own vehicles. Ford Credit Canada’s Newcomer Program accepts PRs, TFWs, and international students. These programs may offer competitive rates on brand-new vehicles.

Best for: Newcomers open to purchasing a new vehicle from a specific manufacturer.

Alternative / Subprime Lenders

If traditional lenders won’t approve you, alternative lenders fill the gap. They offer higher rates (sometimes 15–30%) but provide access to financing that can help you establish credit. Think of it as a bridge — not a permanent solution. (Source: Dilawri)

Best for: Newcomers with irregular income, unusual status, or who’ve been declined elsewhere.

A Real-World Scenario: Maria’s Journey

Maria arrived in Toronto from the Philippines in January 2025 as a permanent resident. She found work as a healthcare aide in Mississauga — a 40-minute commute by transit, but only 15 minutes by car. Her Canadian credit file was empty.

Here’s what she did:

- Month 1–2: Opened an RBC Advantage Banking account (fee-waived for newcomers) and applied for the RBC Cash Back Mastercard.

- Month 3: Started putting her transit costs on the credit card and paying it off every two weeks.

- Month 4: Visited an RBC branch and asked about their newcomer auto loan program. With her employment letter, recent pay stubs, and PR card, she was pre-approved for up to $22,000 at a rate of 9.5%.

- Month 5: Chose a 2021 Honda Civic with 45,000 km, financed $18,500, and put $4,500 down (approximately 20%). Monthly payments: $395 over 60 months.

- Month 18: With consistent payments and active credit card use, her credit score reached 680 — prime territory.

Maria’s story isn’t unusual. The pathway exists — it just requires a clear plan and a bit of patience.

Building Credit After Your Loan: Making the Most of Your Investment

Getting approved is step one. What you do afterward determines your entire Canadian financial future.

Your car loan is a powerful credit-building tool because it’s an installment loan — a type of debt that Canadian credit bureaus (Equifax and TransUnion) weight heavily in your credit score calculation. Every on-time payment is a brick in the foundation of your Canadian credit history.

Here are the habits that matter most:

Pay on time, every time. Even one missed payment can drop your score significantly and stay on your report for up to 6 years. Set up automatic payments from your Canadian bank account to eliminate this risk.

Don’t max out your credit card. Keep your credit utilization below 30% of your credit limit. If your card has a $2,000 limit, try not to carry a balance above $600.

Don’t close old accounts. Length of credit history matters. Keep your bank accounts and credit cards open even if you’re not using them heavily.

Check your credit report regularly. Both Equifax and TransUnion allow you to check your report for free. Review it for errors — reporting mistakes are more common than many people realize, especially for newcomers whose names or addresses may have been entered differently.

Source: Equifax Canada — Understanding Your Credit Report

Source: TransUnion Canada — Credit Education

Common Mistakes Newcomers Make (And How to Avoid Them)

Even well-prepared newcomers fall into some predictable traps. Here’s what to watch for:

Mistake #1: Accepting the first offer

Dealers are motivated to get you financing — but their first offer isn’t always their best. Get a bank pre-approval first, then let the dealer try to beat it.

Mistake #2: Financing a vehicle that’s too old

Many newcomers look for the cheapest car possible, but vehicles over 10 years old often can’t be financed through major lenders — and even if approved, interest rates are higher.

Mistake #3: Ignoring total cost of ownership

Insurance for newcomers in Canada can be higher than expected, especially with no Canadian driving record. Factor in insurance, gas, maintenance, and registration before committing to a monthly payment.

Mistake #4: Multiple hard credit inquiries

Every time you formally apply for credit, a hard inquiry appears on your file. Too many in a short period can lower your score. Rate shop within a focused 14-day window — credit bureaus typically treat multiple auto loan inquiries within this timeframe as a single inquiry.

Mistake #5: Skipping the test drive and inspection

This applies especially to used vehicles. A pre-purchase inspection by an independent mechanic (typically $100–$150) can save you from buying someone else’s problem.

Key Takeaways

Getting approved for a car loan as a newcomer in Canada is absolutely achievable — but it works best when you approach it strategically:

- Major banks like RBC and TD have dedicated newcomer auto programs that don’t require Canadian credit history

- Your immigration status (PR, TFW, international student) determines your eligibility and which programs are available

- A down payment of 15–25% significantly improves your approval odds and reduces your interest rate

- Compare bank programs, dealership financing, and manufacturer programs before committing

- Your car loan is a credit-building opportunity — treat every payment as an investment in your Canadian financial future

- Rate shop within a 14-day window to minimize the impact of hard credit inquiries

- Rates as of 2026 start around 6.50% for well-qualified borrowers; newcomers without history should budget for 9–15% initially

Canada’s roads are waiting. With the right preparation and the right lender, the keys could be in your hand sooner than you think.

Frequently Asked Questions

Can I get a car loan in Canada with no credit history?

Yes. Programs from RBC, TD Auto Finance, Ford Credit Canada, and many dealerships specifically accommodate newcomers with no Canadian credit history. Income verification and a down payment are typically required instead.

Do I need a co-signer for a newcomer car loan?

Not necessarily, but having one can improve your approval odds and reduce your interest rate. A co-signer must have an established Canadian credit history and be willing to take on responsibility for the loan if you default.

How much down payment do I need?

RBC’s newcomer program requires a minimum of 15%. Putting down 20% or more generally improves your rate and makes approval easier across most lenders.

Will my foreign credit history be considered?

Most Canadian lenders do not accept foreign credit history. Some specialized programs may consider it, but it’s the exception rather than the rule. (Source: Vernon Toyota)

How long does it take to get approved?

Through a dealership’s financing department, approval can come within hours. Pre-approval through a bank branch may take 1–3 business days.

Final Thoughts

Moving to Canada is one of the biggest transitions you’ll ever make — and navigating the financial system in a new country adds a whole layer of complexity. But when it comes to auto financing, Canadians are lucky to have a mature market with real options for newcomers.

The system isn’t designed to keep you out. It’s designed to give you a chance — and your job is to show up prepared. Know your documents, understand the lender landscape, save for a meaningful down payment, and treat your first Canadian car loan as the credit-building launching pad it truly is.

At ArriveThenThrive.ca, our mission is to help newcomers navigate exactly these kinds of decisions — with clear, honest, practical guidance grounded in real Canadian experience. Bookmark this page, share it with a fellow newcomer, and reach out if you have questions.

You’ve already made the hard journey. Now let’s get you moving.

Sources & References

- RBC Newcomer Auto Loan Program: https://www.rbcroyalbank.com/new-to-canada/car-loans-for-newcomers/

- TD Auto Finance – New to Canada Program: https://www.td.com/ca/en/personal-banking/products/borrowing/auto-finance/new-to-canada

- Ford Credit Canada Newcomer Program: https://www.ford.ca/finance/special-programs/newcomer-program/

- MoneySense – Auto Loans for Newcomers to Canada: https://www.moneysense.ca/save/financial-planning/newcomers-to-canada/newcomers-auto-loans-buying-a-car-in-canada/

- Finder Canada – Car Loan Interest Rates 2026: https://www.finder.com/ca/car-loans/car-loan-interest-rates

- Hello Motors – Average Auto Loan Rates by Credit Score in Canada (2026): https://hellomotors.ca/blog/average-auto-loan-rates-by-credit-score-in-canada

- Ratehub.ca – Best Car Loans in Canada: https://www.ratehub.ca/loans/best-car-loans

- Dilawri – Subprime Financing for Newcomers: https://www.dilawri.ca/en/news/view/how-newcomers-can-buy-a-car-in-canada-without-credit-using-subprime-financing/149160

- Vernon Toyota – Newcomer Auto Loan FAQ: https://www.vernontoyota.com/newcomer-to-canada

- DeFi Solutions – Canadian Auto Lending Trends 2026: https://defisolutions.com/defi-insight/canadian-auto-lending-market-trends/

- Equifax Canada: https://www.consumer.equifax.ca/personal/education/credit-report/

- TransUnion Canada: https://www.transunion.ca/education

⚠️ Disclaimer

The information provided in this article is for general informational and educational purposes only and does not constitute financial, legal, or lending advice. Auto loan eligibility, interest rates, terms, and program availability are subject to change without notice and vary by lender, province, and individual financial profile. Rates and program details referenced in this article reflect publicly available information as of April 2026 and may no longer be current at the time of reading.

ArriveThenThrive.ca is not a financial institution, mortgage broker, or loan provider, and is not affiliated with any of the lenders mentioned in this article. Readers are strongly encouraged to consult directly with licensed financial professionals or lenders before making any borrowing decisions. Always read the full terms and conditions of any loan agreement before signing.

Individual results will vary. Past approval experiences of others are not a guarantee of your own eligibility or approval outcome.