You’ve packed your life into suitcases, navigated visa paperwork, and finally landed in Canada. You’ve got a SIN number on the way, an address figured out, and a growing to-do list. And somewhere near the top of that list is three words that can feel surprisingly daunting: open a bank account.

Here’s the thing — Canada’s banking system is actually one of the most stable and well-regulated in the world. But it’s also layered. You’ve got the Big 5 banks dominating every major city corner, and then a growing number of online-only banks quietly offering deals that might make your jaw drop. So which do you choose?

In this guide, we break down exactly what Canada’s Big 5 banks and online banks each offer newcomers — including fees, newcomer programs, credit-building opportunities, and the smart strategy many new Canadians are quietly using to get the best of both worlds.

Understanding Canada’s Banking Landscape

Who Are the Big 5 Banks?

Canada’s banking sector is anchored by five major institutions — commonly called the “Big 5”:

- RBC (Royal Bank of Canada) — Canada’s largest bank, with over 1,100 branches and 4,000 ATMs nationwide

- TD (Toronto-Dominion Bank) — Over 1,000 branches, 2,500+ ATMs, and nearly 28 million customers worldwide

- BMO (Bank of Montreal) — Canada’s oldest bank (founded 1817), with nearly 2,000 branches and 5,700+ ATMs

- Scotiabank — Over 25 million customers across the Americas, with strong international ties

- CIBC (Canadian Imperial Bank of Commerce) — A national presence with broad newcomer support programs

You may also hear the term “Big 6,” which includes National Bank of Canada — a major institution with a strong foothold in Quebec and an increasingly competitive newcomer program.

Source: Wealthsimple — Best Banks in Canada Guide

Source: Wealthsimple — Best Banks in Canada Guide

The Rise of Online Banks in Canada

In the past decade, online-only banks — also called digital banks or direct banks — have reshaped what Canadians expect from banking. With no physical branches, these institutions pass their overhead savings directly to customers in the form of higher interest rates and $0 monthly fees.

The top online banks in Canada include:

- EQ Bank — The online arm of Equitable Bank, offering up to 2.75%+ interest on everyday chequing-savings hybrid accounts. Ranked #1 by Forbes in Canada (World’s Best Banks 2025)

- Tangerine — A wholly owned subsidiary of Scotiabank with nearly 2 million clients, offering no-fee chequing and competitive savings rates

- Simplii Financial — CIBC’s digital banking arm, offering no-fee chequing with access to 3,400+ CIBC ATMs

- Neo Financial — A fintech with high-interest savings and cashback rewards, serving 1.3 million+ clients

- KOHO — A hybrid fintech offering up to 3.5% interest on balances with strong budgeting tools

All major online banks mentioned are CDIC (Canada Deposit Insurance Corporation) members, protecting your deposits up to $100,000 CAD per eligible category. Source: CDIC — https://www.cdic.ca

Big 5 Banks vs Online Banks: A Head-to-Head Comparison

Let’s put the two options side by side across the factors that matter most to newcomers.

TABLE 1: Big 5 Banks vs Online Banks — Key Features for Newcomers to Canada

Feature | Big 5 Banks | Online Banks | Best For Newcomers? |

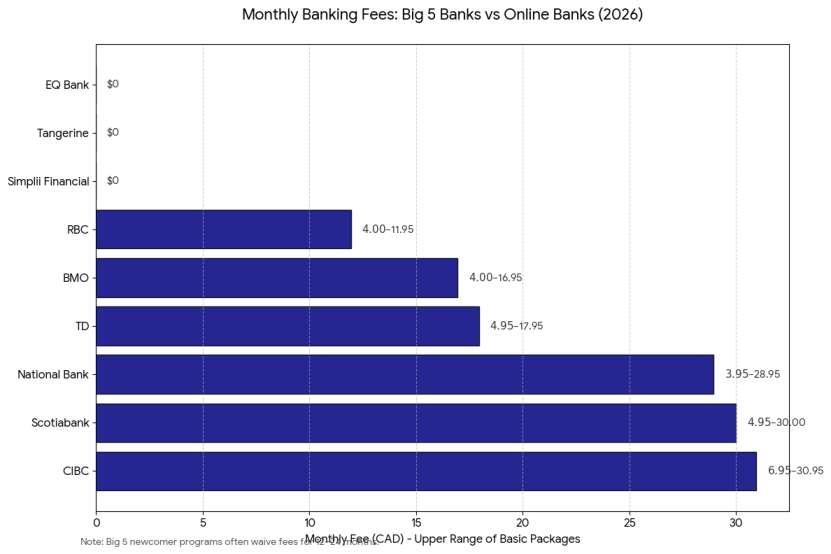

Monthly Fees | $4–$30.95/month | $0 (most) | Online Banks ✓ |

Savings Interest Rate | 0.05%–0.25% | 2.50%–3.50%+ | Online Banks ✓ |

Newcomer Programs | 6–24 months fee waiver | No dedicated programs (most) | Big 5 Banks ✓ |

Physical Branches | 1,000–5,000+ across Canada | None (digital only) | Big 5 Banks ✓ |

ATM Access | Extensive own network | Partner ATMs or fee-free nationwide | Tie |

Credit Building (no history) | Yes – newcomer credit cards | Limited | Big 5 Banks ✓ |

International Transfers | Moderate fees | Lower fees (e.g., EQ + Wise) | Online Banks ✓ |

Pre-Arrival Account Opening | Yes (most Big 5) | Varies | Big 5 Banks ✓ |

CDIC Insured | Yes | Yes (most) | Tie |

Mobile App Quality | Good | Excellent | Online Banks ✓ |

Sources: Wealthsimple, Savvy New Canadians, MoneySense, NerdWallet Canada, EQ Bank official website. Data current as of early 2026; always verify current rates with each institution.

Once the newcomer fee-waiver period at your Big 5 bank ends, you’ll start paying $10–$30 a month just to keep your account open. That’s $120–$360 per year for the privilege of holding your money. Online banks, by contrast, charge nothing — ever.

The Interest Rate Gap Is Real

Here’s where online banks genuinely shine. As of early 2026:

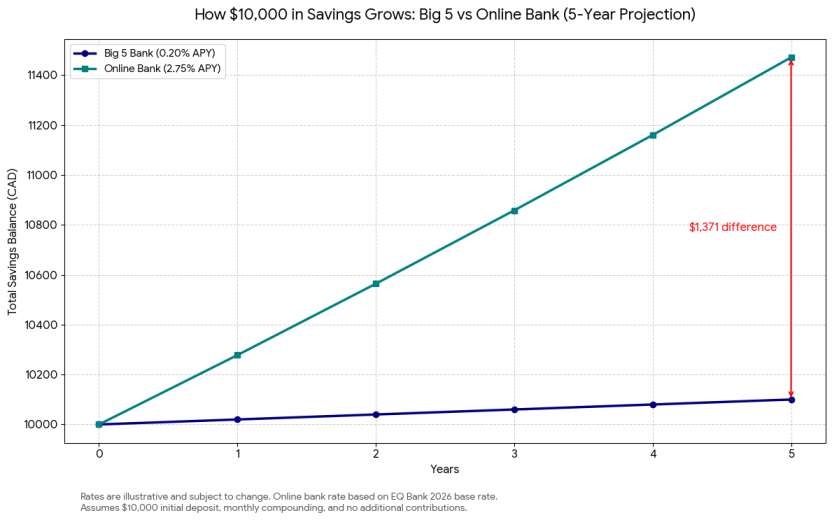

- Big 5 savings accounts typically offer 0.05%–0.25% interest on balances

- EQ Bank’s Personal Account offers 2.75%+ interest — even on everyday chequing balances — when you set up a direct deposit

- Tangerine regularly runs promotional rates of 4%–5% for new customers on savings accounts

- KOHO’s hybrid account offers up to 3.5% interest depending on your subscription tier

The math is simple: if you keep $10,000 in savings, a Big 5 bank might earn you $10–$25 in interest per year. EQ Bank at 2.75% earns you $275. Over five years, that difference compounds significantly.

Source: EQ Bank official website (https://www.eqbank.ca) and NerdWallet Canada — Best High-Interest Savings Accounts 2026

International Money Transfers — Lower Costs with Online Banks

Many newcomers regularly send money back home to family. This is another area where online banks gain ground. EQ Bank partners with Wise (formerly TransferWise) for international money transfers, consistently offering better exchange rates and lower fees than the Big 5’s standard wire transfer fees. According to EQ Bank’s own research (March 2025), their international transfer costs were substantially lower than those of Canada’s Big 5 banks when sending $500 CAD to India, the US, and France.

The Dual-Bank Strategy: What Smart Newcomers Are Doing

Here’s a practical secret that many financially savvy newcomers in Canada quietly figure out — usually after paying Big 5 fees for a year or two: you don’t have to choose just one bank.

The dual-bank strategy works like this:

- Open a Big 5 newcomer account first. Take advantage of the free banking period, use it to build a Canadian credit history with your newcomer credit card, and establish your direct deposit. These first 12–24 months are free anyway.

- Simultaneously, open an online bank account (EQ Bank, Tangerine, or Simplii). Park your savings there to earn significantly higher interest. Use it for bill payments and e-transfers where there are no fees.

- After your newcomer program ends, evaluate. By this point, you’ll understand your banking habits. Some newcomers keep both accounts indefinitely. Others consolidate to the online bank once their credit score is established.

This approach is endorsed by multiple Canadian personal finance sources including Savvy New Canadians and VisaVio Immigration Blog.

The underlying logic is sound: Big 5 banks give you legitimacy, branch access, and credit-building tools in your first critical months. Online banks give you better financial returns once you’re settled. You don’t have to sacrifice either.

Building Credit as a Newcomer: Why Your Bank Choice Matters