You’ve landed in one of the world’s most stable, prosperous countries. But between setting up your bank account, finding a place to live, and navigating a new tax system, investing in real estate is probably the last thing on your mind — and that’s completely understandable.

Here’s the thing, though: Canada’s real estate market has made millionaires out of ordinary people for decades. And as a newcomer, you actually have more options to participate than you might think — even before you qualify for a mortgage, even before you’ve saved up a down payment, and even if you’re still on a work permit.

This guide will walk you through how to invest in Canadian real estate as a newcomer, starting with the most accessible route — REITs (Real Estate Investment Trusts) — and branching out into other smart alternatives that fit a newcomer’s unique financial situation.

By the time you finish reading, you’ll know exactly how to start building real estate wealth in Canada — from as little as $50 — using accounts and vehicles that are already available to you as a new resident.

💡 PRO TIP

Why Real Estate Investing Is So Appealing in Canada — Especially for Newcomers

Canada’s real estate market has one of the strongest long-term track records in the G7. But for newcomers, there’s an even more specific reason the market matters: you are part of the very demand that drives it.

Canada’s federal government has targeted admitting 395,000 new permanent residents in 2025, 380,000 in 2026, and 365,000 in 2027 (Source: IRCC Immigration Levels Plan — canada.ca). Nearly all of Canada’s population growth now comes from immigration, and newcomers overwhelmingly settle in Toronto, Vancouver, and Montreal — the three cities with the tightest rental markets in the country.

What does that mean for you as an investor? It means demand for housing isn’t going anywhere. The Canada Mortgage and Housing Corporation (CMHC) estimates Canada needs 3.5 million more homes by 2030 to restore affordability (source: cmhc-schl.gc.ca). You can either be priced out of that reality, or you can profit from it.

The good news is that you don’t need to buy a house to invest in real estate. Here’s how to start.

What Is a REIT — and Why It’s the Perfect Starting Point for Newcomers

A Real Estate Investment Trust (REIT) is a company that owns and manages a portfolio of income-generating properties — think apartment buildings, shopping centres, warehouses, and office towers. Instead of buying a property yourself, you buy units (shares) in the REIT, which trades on the Toronto Stock Exchange (TSX) just like a stock.

When the REIT collects rent from tenants, it distributes most of that income to unitholders like you, usually monthly. You get exposure to real estate, regular income, and you never have to fix a leaky faucet.

Why REITs Work Especially Well for Newcomers

- No down payment — you can start with as little as $50–$100

- No credit history required — you invest through a brokerage account, not a mortgage

- Available from your first day as a Canadian tax resident

- Can be held inside a TFSA for completely tax-free growth and income

- Highly liquid — you can sell your units the same day if needed

- Professionally managed — no landlord responsibilities

For someone still building their Canadian credit score, financial history, and emergency fund, a REIT is the ideal bridge investment — it gives you real estate exposure today, while you work toward homeownership later.

Top Canadian REITs to Know About

The Canadian REIT sector is well-developed, with publicly traded trusts spanning residential, industrial, retail, and healthcare real estate. Here are some of the most relevant options for newcomers:

Residential REITs — Closest to the Newcomer Experience

Canadian Apartment Properties REIT (CAPREIT) is Canada’s largest publicly traded residential REIT, with over 64,000 units concentrated in Ontario and British Columbia (Source: Globe and Mail — theglobeandmail.com). Its Canadian residential portfolio maintained 97.8% occupancy in Q3 2025, with average monthly rents up 4.4% to $1,709 — a direct reflection of the housing shortage newcomers themselves experience.

Boardwalk REIT focuses on Alberta and Saskatchewan — markets with no rent control and strong population growth. Analysts are watching Boardwalk’s $39M Saskatoon acquisition and growing Prairie exposure (Source: Coldwell Banker Horizon Realty — kelownarealestate.com).

Morguard REIT holds approximately 13,089 residential suites across Canada and the U.S., with FFO payout ratios as low as 40.3% — one of the most conservative and secure distributions in the sector (Source: Motley Fool Canada — fool.ca).

Industrial & Diversified REITs

Granite REIT focuses on logistics and industrial properties — a sector that benefits from e-commerce growth. CT REIT, anchored primarily by Canadian Tire leases, offers a monthly dividend yield of approximately 5.9% with a strong track record of distribution increases (Source: Motley Fool Canada).

TABLE 1: Top Canadian REITs for Newcomer Investors (2025–2026 Snapshot)

REIT | TSX Ticker | Focus | Approx. Yield | Why It’s Relevant for Newcomers |

CAPREIT | CAR.UN | Residential | ~3.5% | Largest residential REIT; 97.8% occupancy |

Boardwalk REIT | BEI.UN | Residential (Prairie) | ~2.2% | No rent control; strong AB/SK growth |

Morguard REIT | MRG.UN | Residential (multi-province) | ~4.3% | Low leverage; secure monthly distribution |

CT REIT | CRT.UN | Retail (Canadian Tire) | ~5.9% | Stable income; patriotic Canadian anchor tenant |

Granite REIT | GRT.UN | Industrial/Logistics | ~4.1% | E-commerce driven; diversified global portfolio |

SmartCentres REIT | SRU.UN | Mixed-Use/Retail | ~7.5% | Mixed-use developments; high yield for income seekers |

Note: Yields are approximate and subject to change. Always verify current figures on the TSX or the REIT’s investor relations page. This table is for educational purposes only.

The Smartest Account to Hold Your REITs In: The TFSA

If you’re going to invest in REITs as a newcomer, you want to do it inside a Tax-Free Savings Account (TFSA). Here’s why this matters so much.

REIT distributions are taxed differently than regular dividends — they come from a mix of return of capital, eligible dividends, capital gains, and ordinary income. In a non-registered account, this creates a reporting headache and a tax bill. Inside a TFSA, all of that growth and income is completely tax-free.

Even better: as a newcomer, you can open a TFSA on your very first day as a Canadian tax resident, with a valid SIN. Your contribution room starts accumulating from the calendar year you become a resident (Source: Canada.ca — canada.ca/en/revenue-agency/services/tax/individuals/topics/tax-free-savings-account).

The 2025 and 2026 TFSA annual limit is $7,000. If you arrived in 2023, you currently have $21,000 in available TFSA room as of January 1, 2026 (see our detailed TFSA guide at arrivethenthrive.ca for your exact room based on arrival year).

Many newcomers don’t realize that TFSA withdrawals don’t count as income. This means your REIT distributions won’t reduce your eligibility for the Canada Child Benefit, GST/HST Credit, or other income-tested benefits. That’s a major advantage unique to the TFSA.

💡 PRO TIP

REIT ETFs: An Even Simpler Way to Diversify

If picking individual REITs feels overwhelming, there’s an even easier option: REIT ETFs. These are exchange-traded funds that hold a basket of Canadian REITs, giving you instant diversification with a single purchase.

The most commonly used option is the iShares S&P/TSX Capped REIT Index ETF (TSX: XRE). It holds a diversified portfolio of the largest publicly traded Canadian REITs, charges a low management fee, and trades on the TSX like any stock. For newcomers who want simplicity without sacrificing exposure, XRE or similar REIT ETFs are an excellent starting point.

The BMO Equal Weight REITs Index ETF (TSX: ZRE) is another popular option, weighting REITs equally rather than by market cap — which means less concentration in the largest names and more balanced sector exposure.

TABLE 2: REIT ETFs vs. Individual REITs vs. Rental Property — Newcomer Comparison

Feature | REIT ETFs (e.g. XRE) | Individual REITs | Rental Property | REIT in TFSA |

Minimum Investment | ~$20–$50/unit | ~$10–$80/unit | $50,000+ down payment | ~$20–$80/unit |

Credit Score Required? | No | No | Yes (typically 680+) | No |

Available Day 1 in Canada? | Yes | Yes | Unlikely | Yes |

Tax-Free Growth Possible? | Yes (in TFSA) | Yes (in TFSA) | No | Yes |

Diversification | High (10–20 REITs) | Low (1 property type) | Very Low (1 property) | High |

Liquidity | Same-day sell | Same-day sell | Months to sell | Same-day sell |

Passive Income? | Yes (monthly) | Yes (monthly) | Yes (but active) | Yes (monthly) |

Landlord Duties? | None | None | Yes | None |

Source: Compiled from Wealthsimple (wealthsimple.com), MoneySense (moneysense.ca), and Million Dollar Journey (milliondollarjourney.com). For educational purposes only.

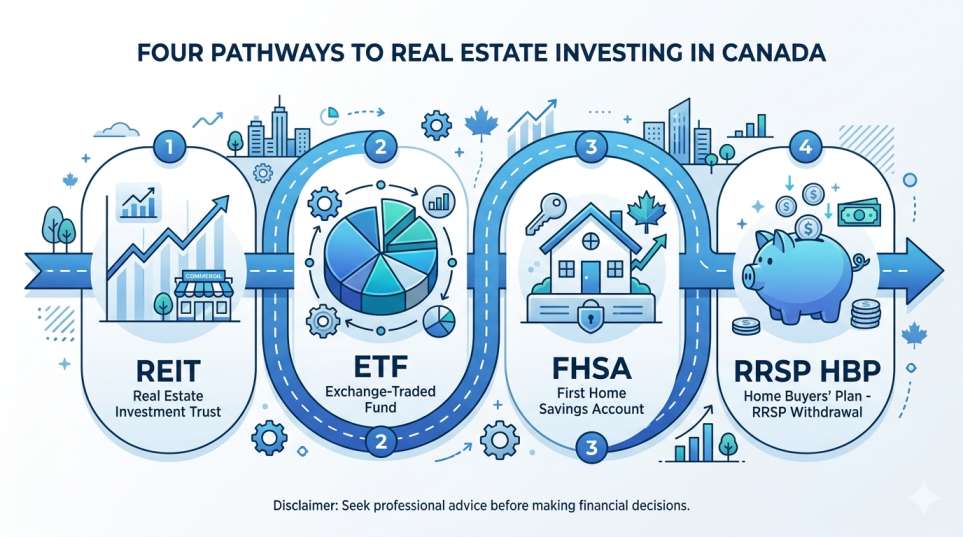

Beyond REITs: Other Real Estate Investment Alternatives for Newcomers

REITs are the most accessible option, but they’re not the only game in town. As your financial footing grows in Canada, here are other real estate investment paths worth understanding.

1. Real Estate Stocks

Some companies listed on the TSX operate in real estate without being structured as REITs — think mortgage lenders, property developers, and real estate technology companies. These are taxed differently (regular capital gains and dividends) and don’t have the same distribution requirements. Examples include FirstService Corporation and Colliers International.

2. The First Home Savings Account (FHSA)

If homeownership is on your horizon, Canada’s First Home Savings Account is a powerful tool unique to first-time buyers. Contributions are tax-deductible like an RRSP, and withdrawals for a first home purchase are tax-free like a TFSA — you get both benefits. You can contribute up to $8,000 per year to a maximum lifetime total of $40,000. As a newcomer, you’re eligible as long as you’re a Canadian resident, have a valid SIN, and have never owned a home in Canada (or in the preceding four years) (Source: Canada.ca).

3. The RRSP Home Buyers’ Plan (HBP)

Once you’ve built RRSP room through Canadian employment income, the Home Buyers’ Plan lets you withdraw up to $35,000 from your RRSP tax-free to use toward your first home down payment. The funds must be repaid to your RRSP within 15 years. Combined with the FHSA ($40,000) and savings ($X), a dual-income newcomer couple could access up to $150,000 in tax-sheltered down payment funds.

4. Private REITs

Private REITs are not traded on stock exchanges and are typically accessible to accredited investors (those with $1M+ in investable assets or $200,000+ in annual income). They may offer higher yields and lower market volatility than publicly traded REITs, but they come with lower liquidity and less regulatory oversight. Companies like Skyline Group of Companies offer private REIT structures in Canada.

5. Pre-Construction Condos (With Caution)

Some newcomers with capital from their home country explore pre-construction condo investment in cities like Toronto or Calgary. This involves putting down a deposit on a unit that won’t be built for 3–5 years, with the intention of selling (assigning) the contract or renting the unit on completion. This strategy carries significant risks — construction delays, market shifts, assignment restrictions, and financing uncertainty — and should only be pursued with expert legal and financial advice.

The key takeaway: Canadian REITs delivered 11.8% total returns in 2025, outperforming the 8.3% global REIT benchmark — the sector’s best year since 2021 (Source: Coldwell Banker Horizon Realty). Meanwhile, the S&P/TSX Capped REIT Index remains below its pre-COVID highs, suggesting a potential recovery opportunity for patient, long-term investors.

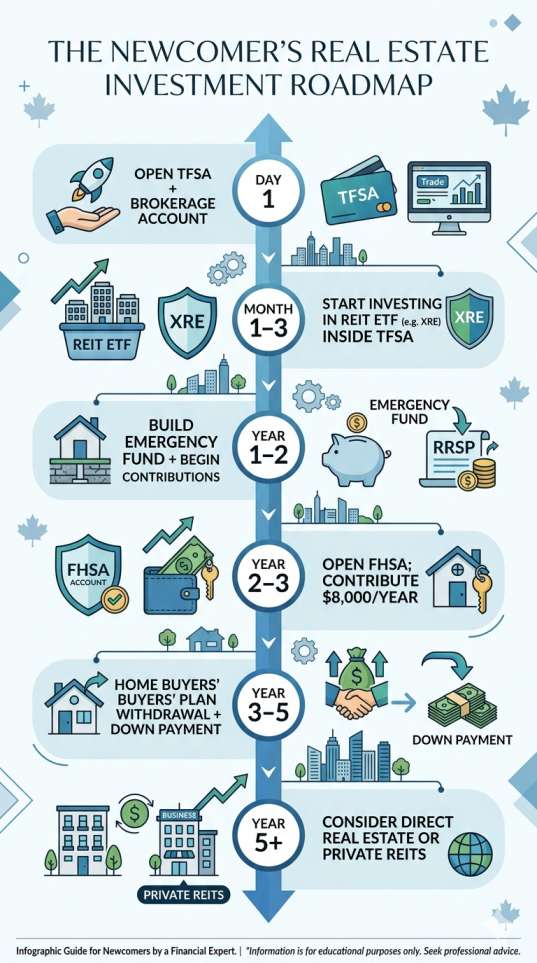

A Real-World Newcomer Scenario: What This Looks Like in Practice

Let’s put this all together with a realistic example.

Amara arrived in Toronto from Nigeria in January 2024 on a work permit, transitioning to permanent residence in early 2025. She earns $72,000/year as a project coordinator. She has no Canadian credit history, no mortgage eligibility yet, and $15,000 in savings she brought from home.

Here’s what Amara’s real estate investment strategy looks like:

- January 2024: Opens a TFSA with Wealthsimple and purchases $7,000 of XRE (iShares REIT ETF) — her full 2024 TFSA room

- January 2025: Contributes another $7,000 to her TFSA, adding CAPREIT units (CAR.UN) for residential exposure

- March 2025: Opens an FHSA and begins contributing $8,000 per year, deducting it from her taxable income

- End of 2025: Her TFSA has grown to ~$15,800 (including REIT distributions reinvested), all completely tax-free

- 2026 Goal: Add $7,000 TFSA + $8,000 FHSA = $15,000 invested in one year while also building her credit score toward future mortgage eligibility

In five years, Amara could potentially have $75,000–$90,000 in a combination of TFSA REITs and FHSA savings — enough for a meaningful down payment on a condo or townhouse — all while having earned tax-free investment income along the way.

The point isn’t the exact numbers. It’s that this strategy is available to you right now, regardless of where you are in your Canadian journey.

Key Tax Considerations for Newcomer Real Estate Investors

Tax rules in Canada are different from most countries, and it’s worth understanding the basics before you invest.

REIT Distributions and Tax Reporting

REIT distributions are reported on a T3 slip (not a T5), and they’re broken down into different income types — eligible dividends, capital gains, return of capital, and ordinary income. Each is taxed differently. This is why holding REITs inside a TFSA is so powerful: you skip all of this complexity entirely.

Non-Residents and REITs

If you’re still a non-resident of Canada (e.g., on a visitor visa or just arrived), you cannot contribute to a TFSA. However, once you’re a Canadian tax resident, your TFSA room begins accumulating in that calendar year. Always verify your residency status with a tax professional.

The Foreign Income Question

If you invest in REITs through a non-registered account and you’re also a tax resident of another country (e.g., a U.S. citizen living in Canada), you may face additional reporting obligations in both countries. Always seek cross-border tax advice in this situation.

Your Newcomer Real Estate Investing Checklist

- Step 1: Get your Social Insurance Number (SIN) — this is required to open any registered account in Canada

- Step 2: Open a TFSA through a bank or online brokerage (Wealthsimple, Questrade, or any Big 5 bank)

- Step 3: Purchase a REIT ETF (like XRE or ZRE) inside your TFSA for instant, diversified real estate exposure

- Step 4: Set up automatic monthly contributions — even $100–$200/month compounds significantly over time

- Step 5: Once you have Canadian employment income for a full year, consider opening an RRSP

- Step 6: Open a First Home Savings Account (FHSA) if homeownership is a goal within the next 15 years

- Step 7: Consult a fee-only financial advisor familiar with newcomer situations before making larger investments

Conclusion: You Don’t Have to Own a House to Invest in Canadian Real Estate

One of the biggest misconceptions newcomers carry is that real estate investing in Canada means buying property — and that’s off the table until they’ve been here for years. That’s simply not true.

REITs and REIT ETFs let you participate in Canada’s housing demand story from day one. The same market forces that make renting expensive in Toronto or Vancouver — immigration, housing shortages, limited supply — are exactly the forces that make residential REITs like CAPREIT strong long-term investments.

As a newcomer, you’re in a unique position: you understand firsthand the housing pressures that drive this market, and you now have access to the tax-sheltered accounts (TFSA, FHSA, RRSP) that make investing in that market highly efficient.

Start small. Stay consistent. And let Canada’s real estate market work for you — not just against you.

Disclaimer

The information provided in this article is for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice. ArriveThenThrive.ca is not a licensed financial advisor, investment dealer, or tax professional. All investments carry risk, including the potential loss of principal. REIT distributions, yields, and performance figures referenced in this article are approximate and based on publicly available information as of early 2026; they are subject to change and may not reflect current market conditions. Past performance of any investment does not guarantee future results. Tax rules in Canada can be complex and vary based on individual circumstances, residency status, country of origin, and applicable tax treaties. Always consult a qualified financial advisor, tax professional, or lawyer before making investment decisions. This article contains links to third-party websites for reference purposes only; ArriveThenThrive.ca is not responsible for the accuracy or content of external sites.